By Ethan Bae | Settle Rich

Ethereum has not looked like a market leader lately. The price action has been frustrating, sentiment has cooled, and even large institutions have turned more cautious. Citigroup recently cut its 12-month Ether target from $4,304 to $3,175, pointing to weak user activity and slower progress on U.S. crypto legislation. At the same time, Citi still noted that growing interest in stablecoins and tokenization could help support Ethereum usage over time.

That is why I think the Ethereum debate in 2026 is more interesting than it looks on the surface.

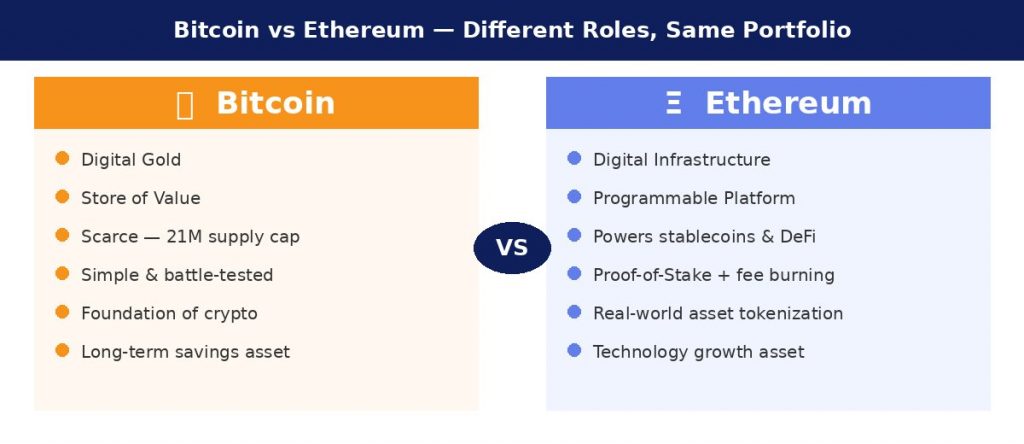

I hold Ethereum directly — not through an ETF, but as actual ETH that I am currently staking. That means I have skin in the game, and I think that context matters when reading anything I write about Ethereum. For context on how I approach Bitcoin differently: I buy a portion of my annual TFSA room in a Canadian-listed Bitcoin ETF on a regular DCA schedule. Same asset class, very different approach. The reason comes down to what each asset is actually for.

The Bearish Case Is Easy to Understand

The bearish case is easy to understand. If you only look at momentum, Ethereum does not look exciting. It is no longer enough to say “Ethereum has the biggest ecosystem” and expect the market to reward that narrative automatically. The market wants visible growth, rising activity, and clear reasons for why ETH itself should become more valuable. On that front, the skepticism is not irrational.

But I also think many investors are making a mistake.

They are looking at Ethereum mainly through short-term price action, when the more important question is whether Ethereum is still one of the core settlement layers for on-chain finance. And I think the answer to that is still yes.

Stablecoins: The Strongest Part of the Ethereum Thesis

Stablecoins are one reason. Ethereum’s own documentation describes stablecoins as Ethereum-based tokens designed to hold a steady value, and they remain one of the clearest real-world use cases in crypto. More importantly, current on-chain data still shows Ethereum as a major stablecoin network: RWA.xyz currently tracks about $168 billion in stablecoin market cap on Ethereum, with more than 22 million holders.

That does not automatically make ETH bullish tomorrow morning, but it does support the idea that Ethereum remains deeply embedded in how digital dollars move on-chain.

Tokenization: Where the Long-Term Case Gets Interesting

This is where the long-term case gets more interesting. According to RWA.xyz, Ethereum currently leads tracked tokenized real-world assets by network, with roughly $16.1 billion in value and about 56% market share. In other words, when real-world assets move on-chain, Ethereum is still taking a large share of that activity.

And the regulatory environment around tokenized securities looks more serious than it did a year ago. In January, the SEC published a statement on tokenized securities to help market participants comply with securities laws. In March, Reuters reported that U.S. regulators said banks would not face extra capital charges simply because securities were tokenized. Reuters also reported that Nasdaq received SEC approval for trading and settlement of certain tokenized stocks and ETFs. Those are not small developments. They suggest tokenization is moving closer to mainstream financial infrastructure rather than staying a niche crypto experiment.

Not Every Crypto App Is Equally Bullish for ETH

That does not mean the bullish case is complete.

A lot of crypto activity is still not especially helpful for ETH price. Polymarket is a good example. People often assume that if a popular app in the broader Ethereum ecosystem grows, ETH should benefit directly. But Polymarket’s own documentation says its contracts are deployed on Polygon mainnet, its markets use USDC.e on Polygon as collateral, and its relayer can enable gasless transactions so users do not necessarily need to hold POL for fees either. Polygon itself describes Polygon PoS as an EVM-compatible sidechain for Ethereum, so there is definitely a relationship to Ethereum, but it is still a weak direct demand driver for ETH.

That distinction matters.

Not every successful crypto application is equally bullish for ETH. If an app grows on a sidechain or another execution layer while using stablecoins as the main transactional asset, the benefit to Ethereum may be more strategic than monetary. It can strengthen the ecosystem without creating strong direct buy pressure on ETH itself.

What Actually Matters: ETH as the Base Layer

So what actually would matter more?

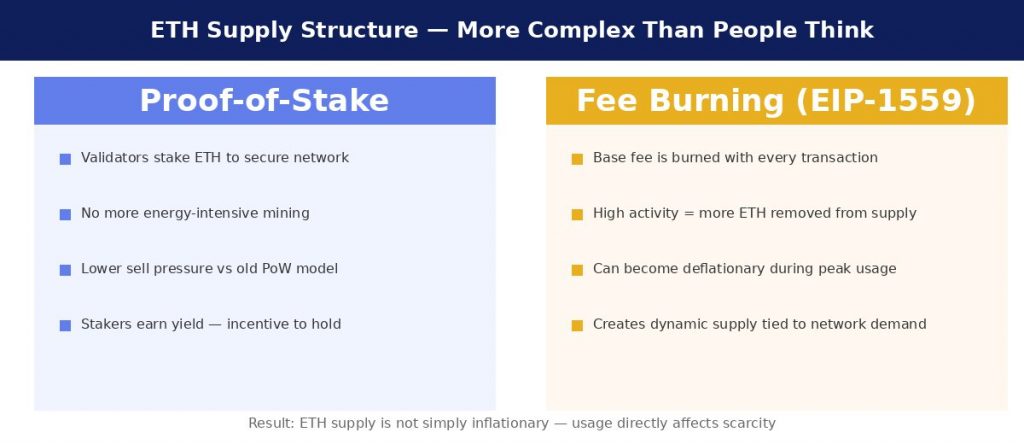

The answer is simple: activity that makes Ethereum the indispensable economic base layer. Ethereum’s documentation explains that every transaction on Ethereum requires fees in ETH, even when the token being moved is something else like USDC or DAI. Ethereum’s scaling roadmap also says that, since the Dencun upgrade, rollups have begun using blob storage and have processed millions of transactions in blobs, reducing costs for users. That is a more meaningful direction for the ETH thesis: more settlement, more data availability demand, more economic activity anchored to Ethereum, and more reasons the network’s native asset remains necessary.

Why I Still Hold — And Stake

This is why I do not think the Ethereum thesis is broken. I think it is incomplete in the minds of many investors.

The weak version of the thesis is: Ethereum should go up because it is important.

The stronger version is: Ethereum still matters because it remains one of the main rails for stablecoins, tokenization, and rollup-based settlement, even if today’s price action does not fully reflect that yet. Those are very different claims. The first is lazy. The second is an actual investment argument.

That is why I have not sold. I hold ETH directly and stake it, collecting yield while I wait. If the infrastructure thesis plays out over the next few years, the patience will be worth it. If it does not, at least the staking rewards soften the wait.

Meanwhile, I keep buying Bitcoin separately — a portion of my TFSA room every year, through a Canadian-listed ETF, on a simple DCA schedule. Bitcoin is my store of value position. Ethereum is my bet on infrastructure. Same asset class, very different roles in the portfolio.

The Bottom Line

In the near term, ETH may continue to lag. That is possible. Weak momentum is real, and disappointing price action should not be ignored. But if stablecoins keep expanding, if tokenized assets keep moving on-chain, and if Ethereum remains the layer where an important share of that economic activity ultimately settles, then the market may be underestimating Ethereum precisely because it is focusing too much on the present and not enough on the infrastructure underneath it.

That is why I still think Ethereum has a case in 2026.

Not because the chart looks strong. Not because the market suddenly owes ETH a rally. But because the deeper role Ethereum plays in on-chain finance may still be more durable than the market currently wants to admit.

This post reflects my personal views and portfolio decisions. It is not financial advice. Always do your own research before investing.