By Ethan Bae | Settle Rich

If you’re a young Canadian trying to build real wealth, the question isn’t just whether to use a TFSA — it’s what to put inside one. The best investments for TFSA Canada aren’t GICs or savings accounts. They’re high-growth assets that turn the account’s tax-free structure into a genuine wealth-building machine.

Most people get this wrong. They open a TFSA, park their money somewhere “safe,” and wonder why their balance barely moves. This post is going to show you exactly why asset selection inside your TFSA matters — and what I would actually put in one if I were starting over in my 20s.

First, a Quick TFSA Refresher (Skip If You Know This)

The Tax-Free Savings Account (TFSA) was introduced by the Canadian government in 2009. Every Canadian resident aged 18+ gets a certain amount of “contribution room” added each year — and any growth inside the account is completely tax-free.

That means no capital gains tax. No dividend tax. No tax when you withdraw. Nothing.

Here’s the full contribution room history:

| Year | Annual Limit | Cumulative Room |

|---|---|---|

| 2009 | $5,000 | $5,000 |

| 2010 | $5,000 | $10,000 |

| 2011 | $5,000 | $15,000 |

| 2012 | $5,000 | $20,000 |

| 2013 | $5,500 | $25,500 |

| 2014 | $5,500 | $31,000 |

| 2015 | $10,000 | $41,000 |

| 2016 | $5,500 | $46,500 |

| 2017 | $5,500 | $52,000 |

| 2018 | $5,500 | $57,500 |

| 2019 | $6,000 | $63,500 |

| 2020 | $6,000 | $69,500 |

| 2021 | $6,000 | $75,500 |

| 2022 | $6,000 | $81,500 |

| 2023 | $6,500 | $88,000 |

| 2024 | $7,000 | $95,000 |

| 2025 | $7,000 | $102,000 |

| 2026 | $7,000 | $109,000 |

If you’ve been eligible since 2009, your total lifetime room is now $109,000.

If you’re completely new to the TFSA and want to understand the basics first, check out our guide: Why You Need a TFSA in Canada — Especially as a Newcomer

You probably know this part. Let’s get to what most people miss.

Why the Best Investments for TFSA Canada Are Growth Assets — Not Savings

Here’s the concept most people don’t fully internalize:

The tax-free benefit scales with your returns.

If your TFSA earns 2% in a high-interest savings account, the government isn’t taxing that 2%. You save maybe $30 in taxes. Fine.

But if your TFSA earns 20%? The government isn’t taxing that either. And now you’re saving thousands — every single year — in taxes you never have to pay.

The bigger the growth, the bigger the tax shield.

This is the core logic behind why the best investments for TFSA Canada are always high-growth assets. A TFSA sitting in a savings account is like owning a Ferrari and only ever driving it in a parking lot. The machine is built for speed. Use it.

The Number That Will Change How You See Your TFSA Forever

Let’s run the actual numbers.

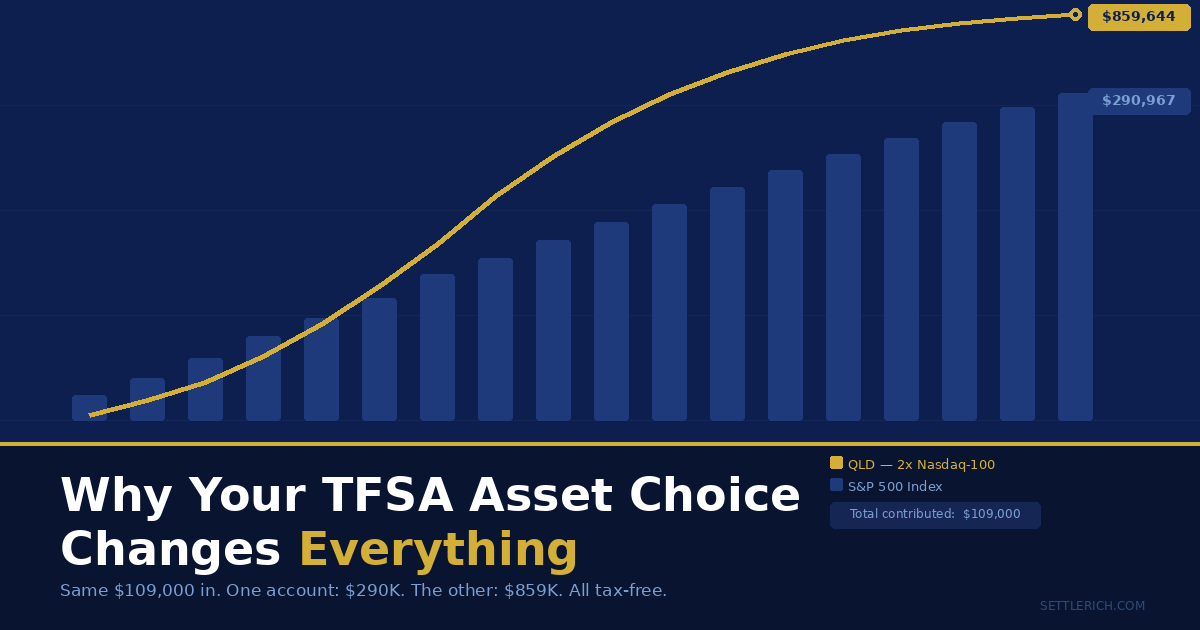

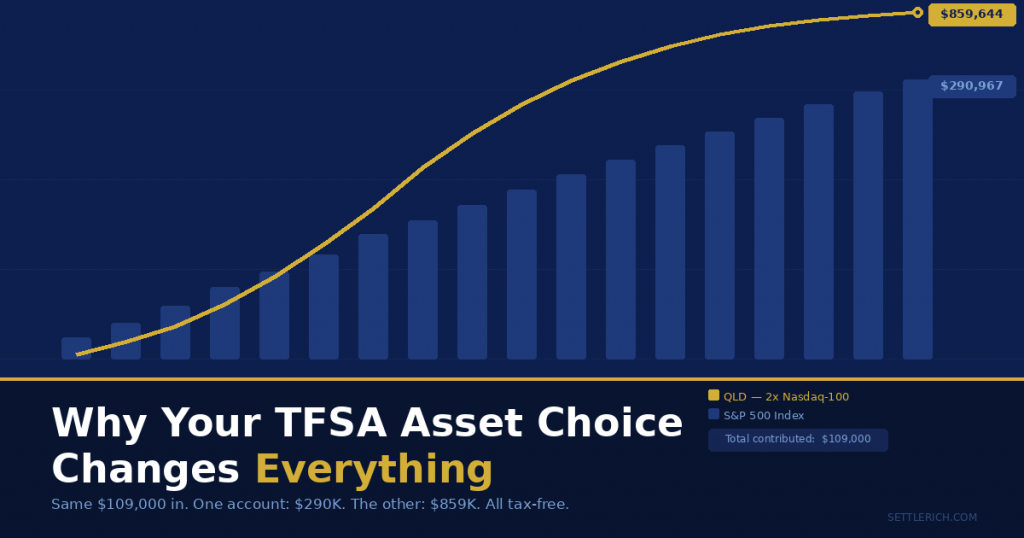

Imagine two investors. Both are Canadian residents who have maxed out their TFSA every single year since 2009 — contributing the full annual limit, every year, without fail. Total contributed: $109,000.

The only difference? What they invested in.

- Investor A put everything into an S&P 500 index fund. Solid, time-tested choice. ~10% average annual return historically.

- Investor B put everything into QLD — a 2x leveraged Nasdaq-100 ETF. Significantly more volatile, but with a historical average annual return closer to ~20% over the long term.

Here’s what happened:

| Year | Contributed | Total In | Investor A (S&P 500) | Investor B (QLD) |

|---|---|---|---|---|

| 2009 | $5,000 | $5,000 | $5,500 | $6,000 |

| 2010 | $5,000 | $10,000 | $11,550 | $13,200 |

| 2011 | $5,000 | $15,000 | $18,205 | $21,840 |

| 2012 | $5,000 | $20,000 | $25,526 | $32,208 |

| 2013 | $5,500 | $25,500 | $34,128 | $45,250 |

| 2014 | $5,500 | $31,000 | $43,591 | $60,900 |

| 2015 | $10,000 | $41,000 | $58,950 | $85,079 |

| 2016 | $5,500 | $46,500 | $70,895 | $108,695 |

| 2017 | $5,500 | $52,000 | $84,034 | $137,034 |

| 2018 | $5,500 | $57,500 | $98,488 | $171,041 |

| 2019 | $6,000 | $63,500 | $114,937 | $212,449 |

| 2020 | $6,000 | $69,500 | $133,030 | $262,139 |

| 2021 | $6,000 | $75,500 | $152,933 | $321,767 |

| 2022 | $6,000 | $81,500 | $174,827 | $393,321 |

| 2023 | $6,500 | $88,000 | $199,459 | $479,785 |

| 2024 | $7,000 | $95,000 | $227,105 | $584,142 |

| 2025 | $7,000 | $102,000 | $257,516 | $709,370 |

| 2026 | $7,000 | $109,000 | $290,967 | $859,644 |

Same money in. Same account. Completely different outcome.

Investor A: $290,967. A solid 2.7x on their money. Respectable — and every dollar of that growth is tax-free.

Investor B: $859,644. Nearly 8x. And every single dollar of that growth? Also completely tax-free.

Over long periods, asset selection can matter just as much as contribution discipline. The same tax shelter, applied to a higher-growth asset, produces dramatically different outcomes. This simulation shows clearly why choosing the best investments for TFSA Canada is a decision worth taking seriously. <!–

The Hidden Superpower: Your TFSA Room Grows With Your Investments

Here’s something most people — even financially savvy ones — don’t fully appreciate.

When you withdraw money from your TFSA, that withdrawal amount gets added back to your contribution room the following January.

This means Investor B doesn’t just have $859,644 in their account. They have $859,644 worth of permanent, tax-free investment space.

If they withdraw everything today and re-contribute next year, they have an $859K tax-free account to work with — for life. That room doesn’t disappear. It compounds with your investments.

Investor A? $290,967 worth of room.

The gap isn’t just in the balance. It’s in the size of your tax-free universe going forward.

If Investor B keeps compounding at 20% per year without adding another cent, that $859,644 becomes:

- $2.1 million in 5 years

- $5.3 million in 10 years

All. Tax. Free.

This is why the best investments for TFSA Canada are the ones with the highest long-term growth potential. You’re not just growing your money — you’re growing the size of your permanent tax shelter.

What About Bitcoin ETF and Ethereum ETF?

This is where it gets interesting for 2025 and beyond.

Canada is one of the few countries in the world where you can hold Bitcoin ETFs and Ethereum ETFs directly inside a TFSA. That means if Bitcoin goes 3x or Ethereum doubles — all of that gain is completely sheltered from tax.

Crypto is one of the most volatile, high-upside asset classes in the world. And you can hold it in a tax-free account. For investors with high risk tolerance, Bitcoin and Ethereum ETFs belong in the conversation about the best investments for TFSA Canada — precisely because the tax-free structure amplifies the upside.

Products like IBIT (iShares Bitcoin ETF, available on Cboe Canada in CAD) give you direct Bitcoin exposure without the complexity of wallets and self-custody — and you can hold it inside your TFSA through platforms like Wealthsimple.

High volatility + high growth potential + tax-free account = a powerful combination for investors who understand the risk they’re taking on.

S&P 500 Is a Great Investment. But It Might Not Change Your Life.

Let me be clear: investing in the S&P 500 is genuinely good. It beats the majority of actively managed funds. It’s diversified. It compounds reliably over decades.

But let’s be honest with ourselves.

If you put $109,000 into an S&P 500 ETF over 18 years and end up with $290,000 — that’s not life-changing money for most people. That’s a solid emergency fund. Maybe a down payment on a condo.

For young investors with long time horizons, the question worth asking is whether that trajectory gets you to where you actually want to go — or just to a comfortable stop along the way.

Without taking on meaningful risk, it’s very hard to meaningfully change your financial trajectory through investing alone.

S&P 500 is the reliable path. And the reliable path, for most people, leads to a comfortable retirement around 65. That’s a genuinely good outcome — if that’s what you’re aiming for.

But if you want something different? The math suggests you need a different asset.

“But Isn’t Leveraged ETF Investing Dangerous?”

Yes. And the honest answer is: it depends entirely on which leveraged ETF and how you hold it.

There’s a meaningful difference between TQQQ (3x leveraged Nasdaq) and QLD (2x leveraged Nasdaq).

TQQQ carries serious long-term risk due to volatility decay — the mathematical drag that occurs when a highly leveraged ETF experiences large swings. When a 3x ETF drops 33%, it needs to gain 50% just to recover. In volatile, sideways markets, this decay can permanently erode your position even if the underlying index eventually recovers.

QLD at 2x is a different proposition. The decay is more manageable, and historically the Nasdaq-100 has trended strongly upward over long periods. Long-term holders of QLD who maintained conviction through drawdowns have seen strong outcomes relative to unleveraged alternatives.

The critical variable is your ability to hold.

QLD has seen brutal drops — during COVID in 2020, during the 2022 rate hike cycle, it fell over 70% at its worst. Investors who sold at the bottom locked in permanent losses. Investors who held — or continued buying — recovered and went on to significantly outperform.

This is not an investment suited to investors who check their portfolio daily and feel sick when it’s red. It’s for investors who understand what they own, believe in the long-term direction of technology and innovation, and have the psychological resilience to hold through extended drawdowns.

If that describes you — QLD inside a TFSA is one of the more powerful wealth-building tools available to a Canadian retail investor.

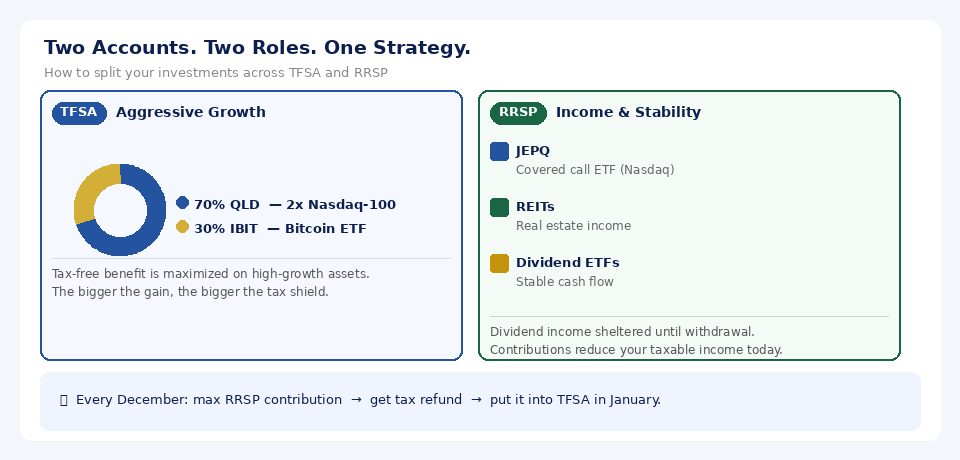

TFSA vs RRSP — Know the Difference and Use Both

Not all registered accounts are the same, and they shouldn’t be used the same way.

The best investments for TFSA Canada — growth assets like QLD and IBIT — belong inside the TFSA because the tax-free benefit is maximized when the growth inside is large.

The RRSP works differently. Contributions reduce your taxable income today, but withdrawals in retirement are taxed as regular income. This makes the RRSP better suited for income-generating, lower-volatility assets — think dividend ETFs, covered call ETFs like JEPQ, or REITs.

Why? Because dividend income earned inside an RRSP is completely sheltered until withdrawal — but if you hold those same dividend assets outside a registered account, you’re paying tax on every distribution, every year.

A simple framework:

- TFSA → Growth assets (QLD, IBIT, Ethereum ETF) — maximize the tax-free compounding on high returns

- RRSP → Income assets (JEPQ, REITs, covered call ETFs) — shelter dividend income and reduce taxable income today

Every December, consider maximizing your RRSP contribution to capture the tax deduction before year-end. The refund you get back can go straight into your TFSA the following January.

I’ll go deeper on the RRSP side in a dedicated post — but the key takeaway: don’t put aggressive growth assets in your RRSP, and don’t waste your TFSA room on conservative income assets.

What I Would Do If I Were in My Early 20s

If I were starting fresh today — 22 years old, new to Canada, building from zero — here’s exactly what I would do:

Every year, I would max out my TFSA contribution. No exceptions.

Then I would invest that money on a monthly DCA (dollar-cost averaging) schedule into two assets:

- 70% QLD — 2x leveraged Nasdaq-100, long-term growth engine

- 30% IBIT — Bitcoin ETF, asymmetric long-term bet

For me, this is the best investments for TFSA Canada strategy for a young person with a long time horizon and genuine risk tolerance. Here’s why:

QLD gives you leveraged exposure to the world’s most dominant technology companies — Apple, Microsoft, Nvidia, Amazon, Google. These are the companies driving the next 20 years of economic growth. At 2x leverage, you’re amplifying that trend while staying within a range that long-term holders have historically been able to manage.

IBIT gives you Bitcoin exposure in the cleanest, most regulated form available. Bitcoin has a fixed supply of 21 million coins. As global money supply keeps expanding — and it has, consistently — Bitcoin’s scarcity becomes more significant over time. The 30% allocation is a high-risk, high-conviction bet. It could underperform significantly. It could also deliver asymmetric returns over a decade.

This is a high-risk allocation. Both assets are volatile. Both require conviction and a long time horizon. But for young investors who understand what they own and can stomach the volatility, this approach gives the best shot at outcomes that actually change your financial life.

Time is your greatest asset. Use it.

Where to Get Started

If you don’t have a TFSA yet — or you’re looking to open one with zero trading commissions — I use Wealthsimple personally.

You can open a TFSA in minutes, buy ETFs like QLD and IBIT with no commission, and set up automatic monthly contributions so the DCA runs on autopilot.

Open a Wealthsimple account here (referral link — we both get a cash bonus)

Final Thoughts

The TFSA is one of the most extraordinary financial tools the Canadian government has ever created. A tax-free account with no expiry date, no income cap, and contribution room that grows every year.

But here’s what most people miss: the TFSA is only as powerful as what you put inside it.

As a young person living in Canada, you have been handed something remarkable. Most countries in the world don’t offer anything like this. No capital gains tax. No dividend tax. No tax on withdrawal. A permanent, growing tax-free investment space that compounds alongside your portfolio.

The best investments for TFSA Canada — growth assets held over decades inside a tax-free account — have the potential to produce outcomes that most investors in the world simply don’t have access to.

This account, used aggressively and consistently over the next 20–30 years, can make you a millionaire without paying a single dollar in tax on your investment gains.

That’s not a marketing line. That’s what the math shows.

The contribution room is there. The assets are accessible. The account is free to open.

What are you waiting for?

Disclaimer: This post is for informational and educational purposes only and does not constitute financial advice. Leveraged ETFs and cryptocurrency ETFs carry significant risk, including the potential loss of principal, and may not be suitable for all investors. Past performance is not indicative of future results. All return figures used in simulations are hypothetical and based on assumed average annual returns — actual results will vary significantly. Please do your own research and consider consulting a qualified financial advisor before making any investment decisions.

Found this useful? Share it with a friend who’s still keeping their TFSA in a savings account. They’ll thank you later.