Most coverage of the CLARITY Act focuses on one simple idea: if the United States finally passes major crypto legislation, institutional money comes in and crypto prices go up.

That may be true in a broad sense. But I think the more important story is somewhere else.

To me, the real issue is not just regulatory clarity. It is the debate around stablecoin yield — and what happens to yield-seeking capital if that door becomes more restricted.

This is not a prediction. It is a thesis. I could be wrong. But I think it is one of the more interesting scenarios investors should be paying attention to.

Where the CLARITY Act Stands

The CLARITY Act has already moved further than many crypto investors expected. It passed the US House with strong bipartisan support, which by itself was a major step.

The bigger challenge has been the Senate.

That is where the conversation has become more complicated, especially around one key issue: whether stablecoin issuers should be allowed to offer yield directly to holders.

That debate matters far more than most people realize.

Because this is not just a technical regulatory detail. It is a question about where billions of dollars in capital may end up going next.

Why Stablecoin Yield Matters So Much

Stablecoins are often described as the “cash layer” of crypto. For many users, they are not just a way to move money quickly. They are also a way to stay in dollar-denominated assets while still participating in the crypto ecosystem.

That matters because many investors do not want to leave crypto entirely just to earn a return on idle capital.

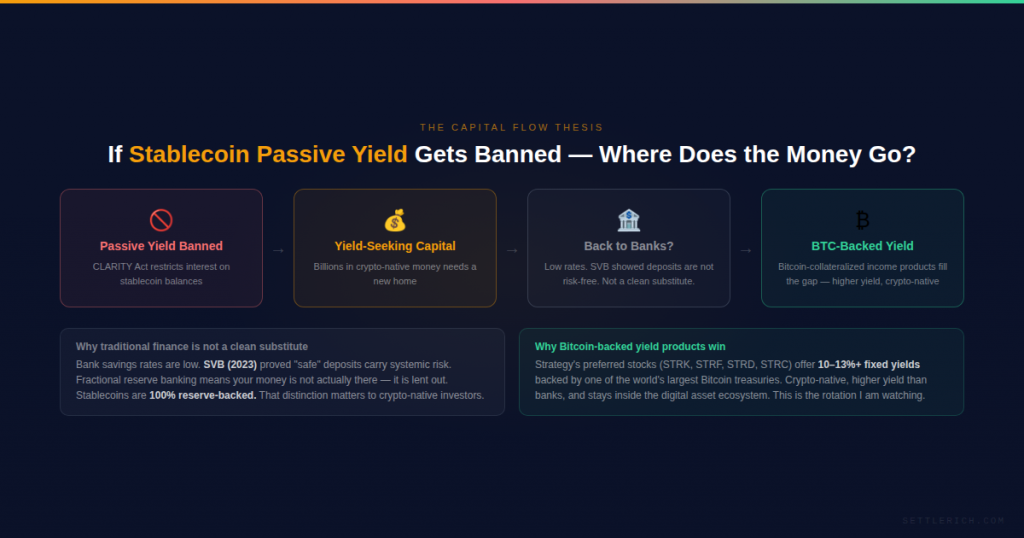

If passive yield on stablecoin balances becomes restricted, that changes the equation.

The question is simple: if investors can no longer earn meaningful passive return on stablecoins, where does that money go?

That is the part I think the market may be underestimating.

My View: Not All of That Capital Goes Back to Traditional Finance

The clarity act crypto discussion often assumes yield-seeking money simply returns to traditional finance — money market funds, Treasury bills, savings products. And some of it will.

But I do not think that is the full story.

A meaningful share of crypto-native capital does not just chase yield. It also cares about the system it is inside. For many crypto investors, moving back into traditional banking products does not feel like a clean substitute. Part of the appeal of stablecoins is not only stability, but also flexibility, transferability, and the ability to stay inside the digital asset economy.

The SVB collapse in 2023 was a reminder that “safe” bank deposits are not actually risk-free. The traditional financial system runs on fractional reserve banking — the bank does not actually hold your money. It lends most of it out. A well-structured stablecoin, by contrast, is 100% backed by reserves. That distinction matters to crypto-native investors.

So if passive stablecoin yield becomes limited, I do not think all of that capital quietly leaves crypto. I think some of it starts looking for the next closest alternative.

Where That Capital Could Move Instead

This is where my thesis becomes more interesting.

If yield on stablecoins becomes harder to access, investors may start paying more attention to products that still offer income while remaining tied, directly or indirectly, to the crypto ecosystem.

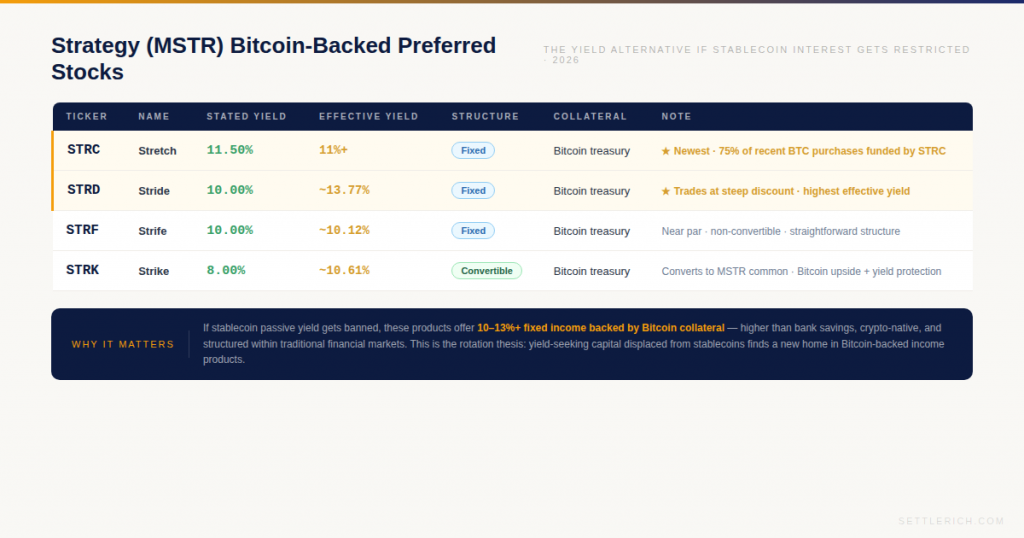

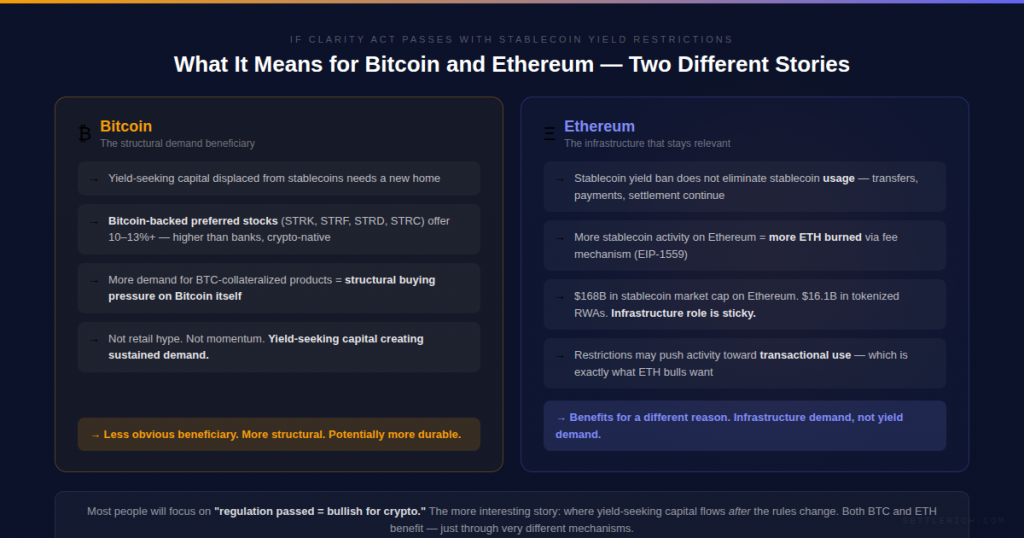

One example is the growing group of preferred securities issued by Strategy — formerly MicroStrategy — such as STRK, STRF, STRD, and STRC. These are not the same thing as holding Bitcoin directly, and they are not simply stablecoin replacements. But they do represent a different kind of yield product connected to a company whose balance sheet is heavily tied to Bitcoin.

STRF offers a 10% fixed annual dividend. STRD mirrors that structure and has been trading at a steeper discount, pushing effective yields toward 13% or higher. STRC, the newest addition, carries an 11.50% stated yield. These are fixed-income products collateralized by one of the largest corporate Bitcoin treasuries in the world — and their yields are meaningfully higher than what traditional bank savings currently offer.

That matters because once yield-seeking investors are pushed out of one corner of crypto, they do not necessarily disappear. They often rotate.

And if that rotation starts, Bitcoin-linked income products could attract more attention than many people expect.

What This Means for Bitcoin and Ethereum

If my thesis is correct, Bitcoin may benefit in a less obvious way.

Most investors think of Bitcoin upside in terms of ETF flows, macro liquidity, or simple price momentum. But another driver could emerge: demand for products that are connected to Bitcoin and designed for yield-oriented capital.

That would matter because it creates a different kind of buyer. Not just the long-term believer. Not just the speculator. But also the investor looking for income exposure tied to Bitcoin-related balance sheets or structures. That kind of demand can become structurally important over time.

Ethereum benefits for a different reason. Even if regulators limit passive yield on stablecoin balances, that does not eliminate the need for settlement, transfers, payments, tokenized assets, and other on-chain activity. Ethereum’s long-term case is tied to usage — and stablecoins remain a massive part of on-chain activity regardless of what the yield rules look like. A stricter stablecoin yield environment may actually push more activity toward transactional use cases, which is exactly what the ETH infrastructure thesis needs.

Where This Thesis Is Weaker

There are a few places where I need to be careful.

First, the CLARITY Act has still not fully become law. That alone means everything discussed here remains scenario analysis, not certainty.

Second, capital does not always move in the neat way investors expect. Some money may leave crypto entirely. Some may rotate into traditional assets. Some may simply stay in stablecoins anyway for convenience, even without yield.

Third, many of the products that could potentially benefit — like Strategy’s preferred stocks — are not equally accessible to every investor, especially outside the United States. So even if the thesis is directionally right, the actual investment pathways may look different depending on where you live.

That is why I see this as a framework for thinking — not a guaranteed outcome.

My Position

Personally, I do not base my Bitcoin or Ethereum exposure on whether the CLARITY Act passes.

I hold Bitcoin because I believe it has a long-term role as a scarce digital monetary asset. I buy a portion of my annual TFSA room in a Canadian-listed Bitcoin ETF on a regular DCA schedule.

I hold Ethereum because I believe it remains one of the most important technology platforms in the digital asset space. I hold it directly as ETH, currently staked.

But if the CLARITY Act does pass with tighter stablecoin yield restrictions, I think the second-order effects could matter more than the headlines.

Most people would focus on the simple story: regulation passed, bullish for crypto.

I think the more interesting story is this: if passive stablecoin yield gets restricted, yield-seeking capital has to move somewhere. And that shift could end up benefiting Bitcoin in ways the market is not fully pricing in yet, while still leaving Ethereum in a strong position as core infrastructure for digital finance.

That is the scenario I am watching. Not just whether regulation is good for crypto. But where capital flows when the rules change.

This article reflects my personal views and investment thesis. It is not financial advice. Regulatory outcomes remain uncertain, and market reactions may differ from the scenario described above. Always do your own research before making investment decisions.